As many Americans log on rather than head to the mall to handle their annual holiday shopping, the growth of consumers utilizing online merchants should be of little surprise to our readers. The proliferation of e-commerce retailing, which has further accelerated since the onset of the global pandemic, is a trend creating a major tailwind for industrial REITs1. An easily overlooked result of this secular change is the amount of distribution infrastructure in superior locations required to support the growth. It is no secret that Amazon is the biggest beneficiary of e-commerce growth, but perhaps less obvious are the benefits reaped by the industrial REIT companies that own the essential real estate infrastructure enabling that.

E-commerce distribution facilities require vast amounts of space, sometimes as much as three times the square footage per unit of sales compared to a brick-and-mortar warehouse/distribution center. Why?

The e-commerce facility:

- is the only place in the supply chain storing inventory in the absence of physical stores,

- has more SKUs (stock-keeping units, the scannable bar codes on product labels),

- is more spread out so employees or robots can locate, pick, and sort goods frequently,

- has more parking,

- needs a large area for returns.2

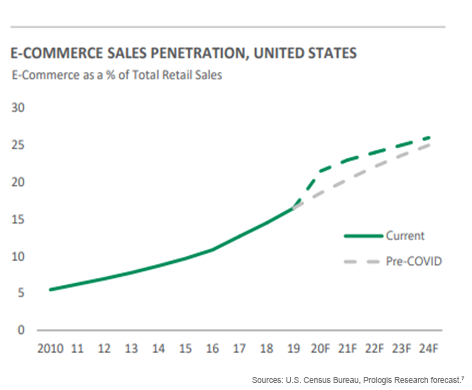

Since e-commerce retailers are engaged in a race to quickly deliver goods to consumers, the supply chain implications are vast. An estimated three billion packages, 36% more than a year ago, will move through the U.S. shipping infrastructure during the 2020 holiday season3. E-commerce sales are approaching 15% of total retail sales and the supply chain is adapting quickly but remains behind due to constraints on space4. Furthermore, many of these packages get returned and require a second move through the entire supply chain.

A few decades ago, most distribution facilities were located in rural areas within a few days drive of population centers. Conversely, today, modern e-commerce facilities are located near major cities, usually within a few hours’ drive from end consumers. These locations have scarcity value5 given limited land availability, zoning challenges, and alternative uses, such as apartments, that command higher rents per square foot. An e-commerce retailer may be willing to pay a premium for the superior location as real estate is typically about 5% of its total operating expenses, which is more than offset by the benefits they reap such as speed to consumer. These locations are typically where industrial REITs such as Prologis and Duke Realty own the real estate6.

At Reaves, we believe that demand for industrial real estate has exceeded supply in recent years, pushing vacancy rates down, and e-commerce retailing is a growing contributor. Record low, mid-single digit vacancy rates have given landlords, such as Prologis and Duke, strong pricing power and allowed national rents to increase at mid-to high-single digit rates throughout the cycle. The pandemic has simply accelerated these trends.

For example, the largest e-commerce retailers are behind on leasing the space needed to meet the growth. Amazon’s CFO recently stated on the company’s second quarter 2020 earnings call on 7/30/20:

“In 2019, we increased network square footage by approximately 15%. This year, we expect a meaningfully higher year-over-year square footage growth of approximately 50%. This includes strong growth in new fulfillment center space as well as sort centers and delivery stations.”

“As we move towards peak in the second half of the year, we will ramp up our space needs even further and we will be adding significant fulfillment center and transportation capacity.”

Industrial REITs currently own, and we expect, will continue to develop the distribution and warehousing infrastructure necessary to accommodate the future growth expected in e-commerce. Their characteristics, including steady growth and superior locations that provide high barriers to entry, are some of the reasons we focus on infrastructure businesses supporting our modern economy. In 2020, shopping from home has truly been elevated to an essential service.

Disclosures:

Reaves Asset Management is an investment adviser registered with the Securities and Exchange Commission under the Investment Advisers Act of 1940. Registration does not imply any skill or training. Reaves is a privately held, independently owned “S” corporation organized under the laws of the State of Delaware.

The information provided in this blog does not constitute, and should not be construed as, investment advice or recommendations with respect to the securities and sectors listed. Investors should consider the investment objective, risks, charges and expenses of all investments carefully before investing. Any projections, outlooks or estimates contained herein are forward looking statements based upon specific assumptions and should not be construed as indicative of any actual events that have occurred or may occur.

1A real estate investment trust (REIT) is a company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors. This makes it possible for individual investors to earn dividends from real estate investments—without having to buy, manage, or finance any properties themselves.

2 https://www.prologis.com/about/logistics-industry-research/global-e-commerce-impact-logistics-real-estate (Section 2 Pages 4-6)

3Corkery, Michael and Maheshwari, Sapna. “With 3 Billion Packages to Go, Online Shopping Faces Tough Holiday Test.” The New York Times, December 5, 2020.

5Scarcity value is an economic factor describing the increase in an item’s relative price by an artificially low supply.

6Reaves Asset Management owned Prologis and Duke Realty as of 9/30/20.

7 See slide 6 of 11/17/20 Prologis presentation: https://s22.q4cdn.com/908661330/files/11/PLD-NAREIT-Virtual-November-2020.pdf

Past performance is no guarantee of future results.

All investments involve risk, including loss of principal.

All data is presented in U.S. dollars.

Important Tax Information: Reaves Asset Management and its employees are not in the business of providing tax or legal advice to taxpayers. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax adviser.