Disclosures:

Reaves Asset Management is an investment adviser registered with the Securities and Exchange Commission under the Investment Advisers Act of 1940. Registration does not imply any skill or training. Reaves is a privately held, independently owned “S” corporation organized under the laws of the State of Delaware.

The information provided in this blog does not constitute, and should not be construed as, investment advice or recommendations with respect to the securities and sectors listed. Investors should consider the investment objective, risks, charges and expenses of all investments carefully before investing. Any projections, outlooks or estimates contained herein are forward looking statements based upon specific assumptions and should not be construed as indicative of any actual events that have occurred or may occur.

1The 10-year Treasury note is a debt obligation issued by the United States government with a maturity of 10 years upon initial issuance. A 10-year Treasury note pays interest at a fixed rate once every six months and pays the face value to the holder at maturity. The U.S. government partially funds itself by issuing 10-year Treasury notes.

2The Bloomberg Barclays US Aggregate Bond Index is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States.

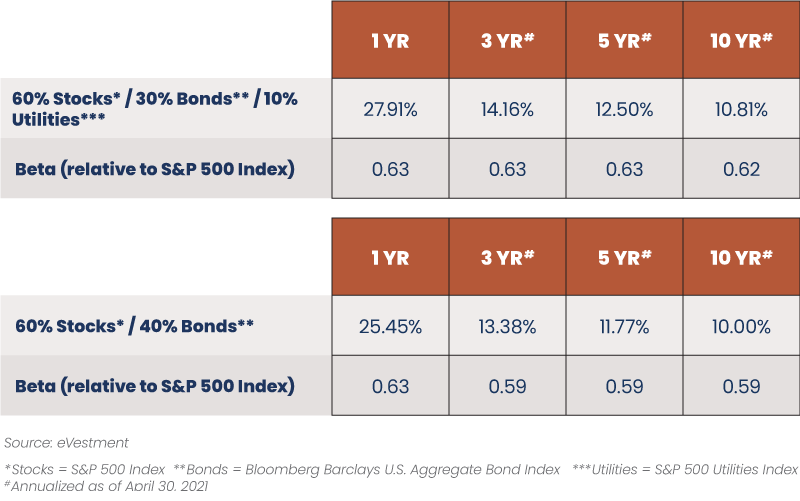

3Source: eVestment. Time period: Ten years ended 4/30/21.

4This is a model portfolio used to represent a specific allocation and is not a product of Reaves.

5Source: eVestment. Time period: Ten years ended 4/30/21.

6The S&P 500 Index (“S&P 500”) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The typical Reaves portfolio includes a significant percentage of assets that are also found in the S&P 500. However, Reaves’ portfolios are far less diversified, resulting in higher sector concentrations than found in the broad-based S&P 500.

7The S&P 500 Utilities Index is a capitalization-weighted index containing electric and gas utility stocks (including multiutilities and independent power producers). Prior to July 1996, this index included telecommunications equities.

8Link to Source: Virtus Reaves Utilities ETF Fact Sheet 1Q 2021

The risk curve is a graphical presentation of the risks and returns of two variables. The risk curve plots two variables on a graph to reflect their financial risks and returns, this graph creates visuals on how returns are made on the assets and the risks entailed. The nature of the risks are also indicated in the graph. The risk curve is made of multiple data representing multiple assets in order to aid the visualization of the relative risks and returns of these assets. The risk curve is an important metric in mean-variance analysis and the Capital Asset Pricing Model.

A defensive stock is a stock that provides consistent dividends and stable earnings regardless of the state of the overall stock market. There is a constant demand for their products, so defensive stocks tend to be more stable during the various phases of the business cycle.

Beta measures a manager’s volatility relative to the market portfolio. A manager with a beta higher than 1.0 has historically been more volatile than the benchmark, while a manager with a beta lower than 1.0 has been less volatile.

You should consider the Fund’s investment objectives, risks, and charges and expenses carefully before investing. Contact Virtus ETF Solutions at 1-888-383-0553 or visit www.reavesetfs.com to obtain a prospectus which contains this and other information about the Fund. The prospectus should be read carefully before investing.

An investment in the Fund is subject to investment risks; therefore you may lose money by investing in the Fund. There can be no assurance that the Fund will be successful in meeting its investment objective. Shares of any ETF are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns. Narrowly focused investments typically exhibit higher volatility.

Specific risks associated with investments in Utility Sector Companies include, without limitation, environmental and conservation considerations, policies and regulations; competition; interest rates; inflation; financing difficulties; technological innovations that may render existing plants, equipment or products obsolete; natural or man-made disasters; costs and availability of services or fuel; changes in taxation; and lengthy delays and greatly increased costs and other problems associated with the design, construction, approval, licensing, regulation and operation of facilities for electric generation, gas production and water treatment and processing.

A downturn in the utilities sectors would have a larger impact on the Fund than on an investment company that does not concentrate solely in Utility Sector Companies.

At times, the performance of companies in the utilities sectors may lag the performance of other sectors or the broader market as a whole. As concentration in a sector increases, so does the potential for fluctuation in the net asset value of the Fund’s shares.

Exchange-Traded Funds (ETF): The value of an ETF may be more volatile than the underlying portfolio of securities it is designed to track. The costs of owning the ETF may exceed the cost of investing directly in the underlying securities.

Equity Securities: The market price of equity securities may be adversely affected by financial market, industry, or issuer-specific events. Focus on a particular style or on small or medium-sized companies may enhance that risk.

Utilities Sector Concentration: The Fund's investments are concentrated in the utilities sector and may present more risks than if the Fund were broadly diversified over numerous sectors of the economy.

Industry/Sector Concentration: A fund that focuses its investments in a particular industry or sector will be more sensitive to conditions that affect that industry or sector than a non-concentrated fund.

Prospectus: For additional information on risks, please see the fund's prospectus Virtus ETF Advisers LLC serves as the investment adviser and W.H. Reaves & Co., Inc. (d/b/a Reaves Asset Management) serves as the investment sub-adviser to the Fund. The Fund is distributed by VP Distributors, LLC.

Not FDIC Insured | Not Bank Guaranteed | May Lose Value.

Past results do not guarantee future performance. Further, the investment return and principal value of an investment will fluctuate; thus, investor’s equity, when liquidated, may be worth more or less than the original cost. This document provides only impersonal advice and/or statistical data and is not intended to meet objectives or suitability requirements of any specific individual or account.

All investments involve risk, including loss of principal.

All data is presented in U.S. dollars.

Cash is cash and cash equivalents.

An investor cannot invest directly in an index.

Important Tax Information: Reaves Asset Management and its employees are not in the business of providing tax or legal advice to taxpayers. Any such taxpayer should seek advice based on the taxpayer’s own individual circumstances from an independent tax adviser.

Fees: Net performance reflects the deduction of advisory fees which are described in detail in our Form ADV Part 2A.

Please contact your financial professional, or click the following links, for a copy of Reaves’ Form ADV Part 2A and Form CRS.

Additional information about Reaves may be found on our website: www.reavesam.com.

2021 © Reaves Asset Management (W. H. Reaves & Co., Inc.)