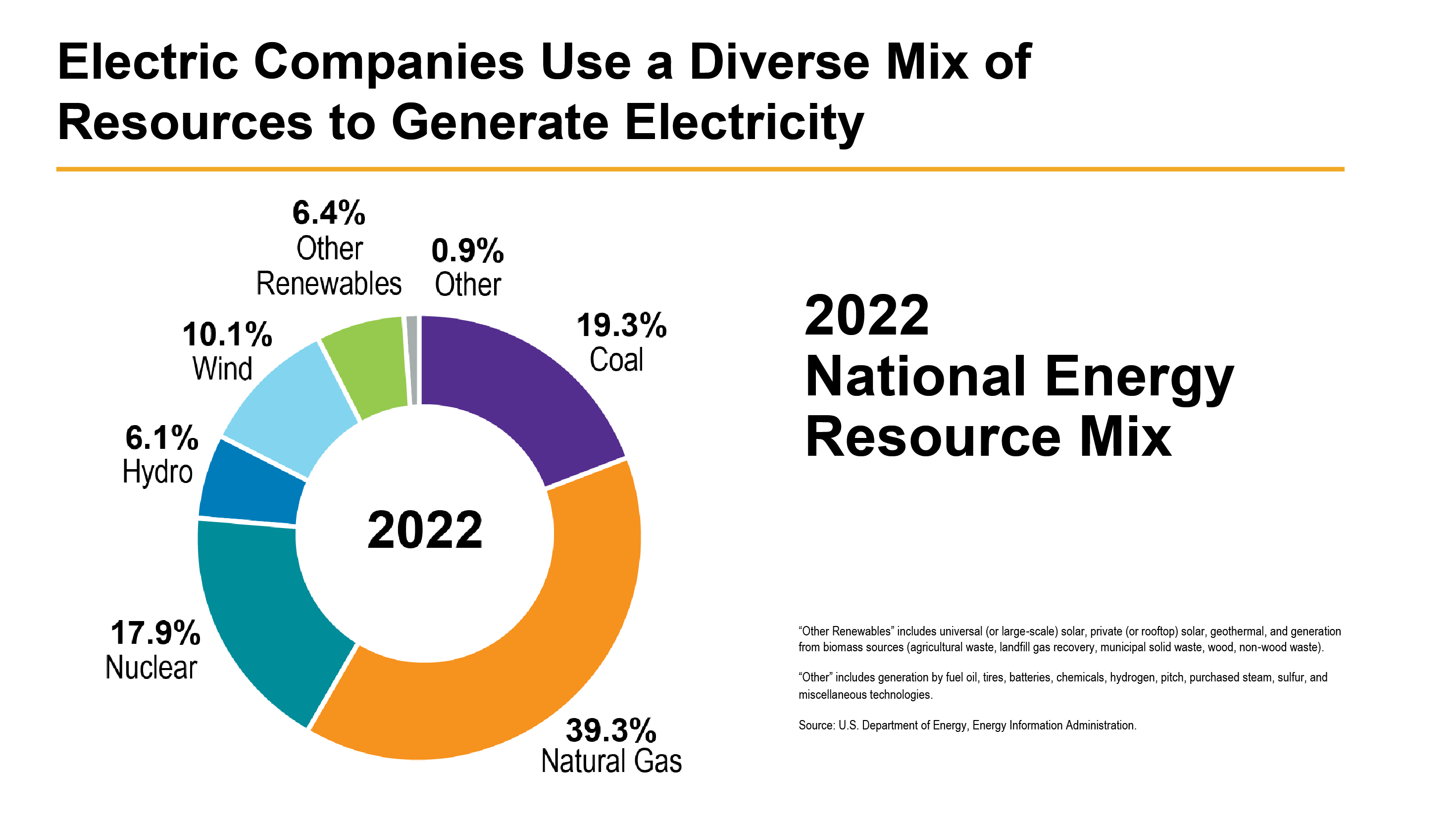

We have highlighted in previous blog posts the long tailwind that the transition to renewable power generation may provide for many utility companies. The more opportunities they have to increase capital expenditures for new infrastructure investments with the consent of regulators, the greater the probability that their rate base will grow. That growth may lead to increases in both earnings and in dividend payments to shareholders. The passage of the Inflation Reduction Act (IRA) last year, with provisions for $270 billion of tax credits to support spending on renewables beyond 2030, may have enhanced the likelihood for many utilities to make such investments.

However, the path forward to a clean energy future will not always be a smooth one. The headline on the cover of the July 24, 2023 edition of Barron’s magazine proclaimed “Trouble In The Wind” and featured an article that documented a variety of issues plaguing offshore wind projects. The Biden administration’s previously stated goal to have 30 gigawatts of offshore wind power capacity in the U.S. by 2030 may be in jeopardy due to a variety of delays related to permitting processes, legal challenges, supply chain issues, and higher costs of construction. Only two offshore wind projects are currently operational off the East Coast of the U.S. with a total of 42 megawatts of generating capacity, a small fraction of onshore wind capacity.

However, the path forward to a clean energy future will not always be a smooth one. The headline on the cover of the July 24, 2023 edition of Barron’s magazine proclaimed “Trouble In The Wind” and featured an article that documented a variety of issues plaguing offshore wind projects. The Biden administration’s previously stated goal to have 30 gigawatts of offshore wind power capacity in the U.S. by 2030 may be in jeopardy due to a variety of delays related to permitting processes, legal challenges, supply chain issues, and higher costs of construction. Only two offshore wind projects are currently operational off the East Coast of the U.S. with a total of 42 megawatts of generating capacity, a small fraction of onshore wind capacity.

At the end of 2022, total global offshore wind capacity was estimated to be 64.3 gigawatts1 with 83% of grid-connected installations located in China, the United Kingdom, and Germany. For perspective, U.S. offshore wind capacity is less than 0.1% of the global total. Several U.S. utility companies have made investments in offshore wind projects, but with little success to date.

Avangrid, a utility company serving 3.3 million electric and gas customers in the Northeast, has a renewables subsidiary which the company website describes as “the third-largest renewable energy company in the U.S. with a diverse onshore and offshore renewable energy portfolio.” However, Avangrid recently agreed to pay $48 million to terminate an offshore wind project because the cost overruns would have led to unacceptable increases in rates charged to their utility customers. This event, combined with a below average regulatory environment in several states in which it operates, helped explain why Avangrid substantially underperformed most other utility stocks over the last three years. Reaves Asset Management has avoided Avangrid over the same period and continues to favor utilities with better regulatory environments and less offshore wind development risks.2

This past May, another New England utility, Eversource Energy, agreed to sell its 50% stake in a wind development site off the south coast of Massachusetts to its joint venture partner Orsted. The sale resulted in Eversource taking a $331 million impairment charge in its recently reported second quarter results. The company’s stock has underperformed most other utilities in the past year. Our investment team’s emphasis on avoiding companies that get involved in riskier ventures was a primary reason we sold Eversource stock from all of our managed accounts more than a year ago above $85 per share. Eversource stock was recently trading at about $68 per share.

We believe onshore wind development carries much lower levels of risk and are currently invested in several utility companies that are developing projects such as Wisconsin Energy, NextEra Energy and Alliant Energy.

Onshore wind farms are far more prevalent in the U.S. today than offshore due to lower costs both for initial construction and ongoing maintenance. Offshore wind farms, however, are generally considered a more reliable and efficient source of generation due to the availability and consistency of offshore wind, especially along the Atlantic coast. Onshore wind speeds generally vary throughout the day and are subject to seasonal fluctuations. The intermittent energy they produce requires fossil-fuel backup for the times when the wind speed slows. This summer, with sea surface temperatures rising due to El Nino conditions in the Pacific, wind speeds are expected to be below average across the country. The impact of wind resource is another factor utility investors must consider when investing in the space.

We are constructive on the potential growth driver the transition to renewable energy may have on the utility sector, but are conscious of the challenges many companies may face. In addition to renewable development risk, every utility’s rate base and regulatory environment are different. Most of the utility companies that we follow have reaffirmed forward earnings guidance in their most recent earnings calls. We continue to believe the outlook remains positive for growth.

Learn more about what we look for when screening utility companies, read the Q&A with portfolio managers Jay Rhame and John Bartlett.