Disclosures and Definitions:

Reaves Asset Management is an investment adviser registered with the Securities and Exchange Commission under the Investment Advisers Act of 1940. Registration does not imply any skill or training. Reaves is a privately held, independently owned “S” corporation organized under the laws of the State of Delaware.

The information provided in this blog does not constitute, and should not be construed as, investment advice or recommendations with respect to the securities and sectors listed. Investors should consider the investment objective, risks, charges and expenses of all investments carefully before investing. Any projections, outlooks or estimates contained herein are forward looking statements based upon specific assumptions and should not be construed as indicative of any actual events that have occurred or may occur.

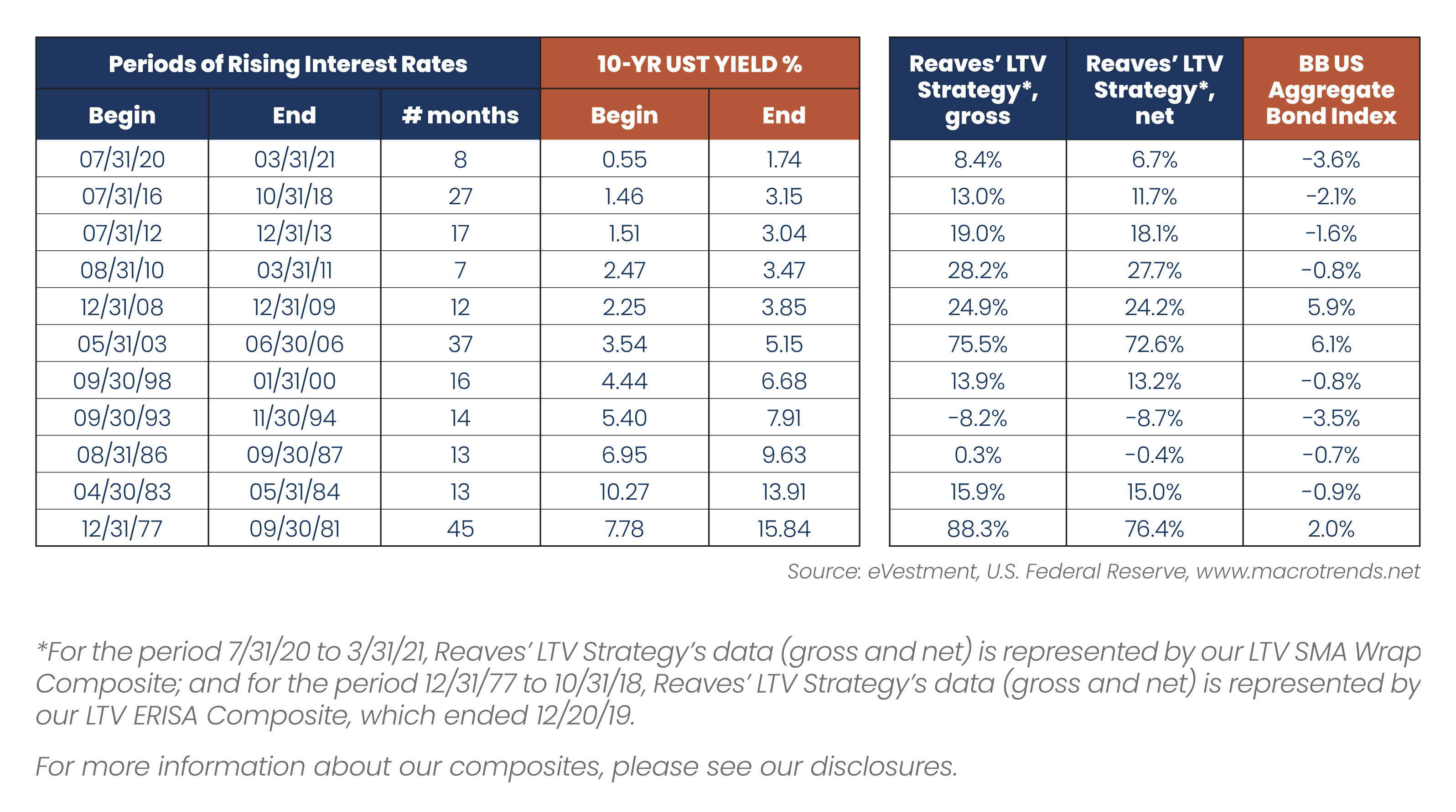

1The Bloomberg Barclays U.S. Aggregate Bond Index is an index comprised of approximately 6,000 publicly traded bonds including U.S. Government, mortgage-backed, corporate, and Yankee bonds with an approximate average maturity of 10 years.

2Reaves’ Long Term Value Strategy (Reaves LTV Strategy) seeks a high risk-adjusted total return. The strategy tends to be invested in relatively larger companies with strong balance sheets, good cash flow and a history of dividend growth. Core positions are accumulated in financially strong, high-quality companies and generally have the following characteristics: strong management, above industry-average growth rates, large/mid-market capitalization and low price-earnings multiples.

Reaves performance data is the Reaves LTV ERISA Composite and, unless otherwise noted, all data is net of fees. The Reaves LTV ERISA Composite reflects the dollar-weighted return of all corporate ERISA pension accounts with assets of at least $1,000,000 under management for all periods presented (the minimum was $900,000 during the period 08/31/10-06/22/12). Returns are time-weighted and include the reinvestment of all dividends and other earnings, net of commissions. The LTV ERISA Composite does not reflect all of the Reaves’ assets under management. The LTV ERISA Composite began on 01/01/78 and ended on 12/20/19.

Beginning December 2019, Reaves LTV Strategy is represented by the LTV SMA Wrap Composite. This composite contains those LTV discretionary portfolios with wrap (bundled) fees. Wrap accounts are charged a bundled fee which includes the wrap sponsor fee, as well as, Reaves’ investment advisory fee. Due to compliance requirements, the net-of-fees calculation is computed based on the highest annual fee assigned by any wrap sponsor who utilizes this portfolio in an investment wrap program (300 basis points from 1/1/03 through 12/31/16 and, effective 1/1/2017, 250 basis points). The LTV SMA Wrap Composite performance consists of money-weighted, time-weighted returns and it includes the reinvestment of all dividends and other earnings. The inception date of the composite is December 2002; however, the composite was created in January 2013. This composite has been managed in a similar manner to the LTV ERISA Composite which ended in December of 2019. The LTV SMA Wrap Composite does not represent all of Reaves’ assets under management.

The 10-Year U.S. Treasury Note (UST) is a debt obligation issued by the United States government with a maturity of 10 years upon initial issuance. A 10-Year U.S. Treasury Note pays interest at a fixed rate once every six months and pays the face value to the holder at maturity. The U.S. government partially funds itself by issuing 10-Year U.S. Treasury Notes.

Past results do not guarantee future performance. Further, the investment return and principal value of an investment will fluctuate; thus, investor’s equity, when liquidated, may be worth more or less than the original cost. This document provides only impersonal advice and/or statistical data and is not intended to meet objectives or suitability requirements of any specific individual or account.

All investments involve risk, including loss of principal.

All data is presented in U.S. dollars.

Cash is cash and cash equivalents.

An investor cannot invest directly in an index.

Important Tax Information: Reaves Asset Management and its employees are not in the business of providing tax or legal advice to taxpayers. Any such taxpayer should seek advice based on the taxpayer’s own individual circumstances from an independent tax adviser.

Fees: Net performance reflects the deduction of advisory fees which are described in detail in our Form ADV Part 2A.

Please contact your financial professional, or click the following links, for a copy of Reaves’ Form ADV Part 2A and Form CRS.

Additional information about Reaves may be found on our website: www.reavesam.com.

2021 © Reaves Asset Management (W. H. Reaves & Co., Inc.)