The U.S. Department of Labor reported last month that the Consumer Price Index rose by 6.2% in the previous 12 month period, its largest annual increase since 1990.1 In response, Federal Reserve Chairman Jerome Powell commented: “At this point, the economy is very strong and inflationary pressures are higher, and it is therefore appropriate in my view to consider wrapping up the taper of our asset purchases, which we actually announced at the November meeting, perhaps a few months sooner.”2 If inflation persists and puts upward pressure on interest rates, we believe investors should be reviewing their asset allocations.

For perspective, interest rates remain lower than the historical average, even with the increase in rates over the past year. The 10-year U.S. Treasury yield has averaged approximately 3.0% over the past 20 years compared to its current level around 1.5%, illustrating that rates have ample room to move higher if the Fed decides to act against inflation and still be well within the recent historical range.

Returns from fixed income investments are likely to face challenges if rates continue higher. The table below displays the cumulative returns of the Bloomberg Barclays U.S. Aggregate Bond Index in the six rising rate environments since 2001.

Sources: eVestment, U.S. Federal Reserve, www.macrotrends.net

For more information, please see our disclosures.

Given prospects for low returns, are fixed income allocations too high?

This is where defensive equities could play a role for investors. By taking a portion of a diversified portfolio’s fixed income allocation and investing it in stocks with defensive characteristics, investors may be able to improve their returns relative to the traditional 60/40 mix, while only slightly altering the portfolio’s risk profile.

We believe our investment strategies deserve consideration in the current market environment. Our own brand of defensive equities — essential service infrastructure stocks — have not only provided defensive characteristics but also may serve as an alternative to bonds in rising rate environments — the key risk facing bonds today.

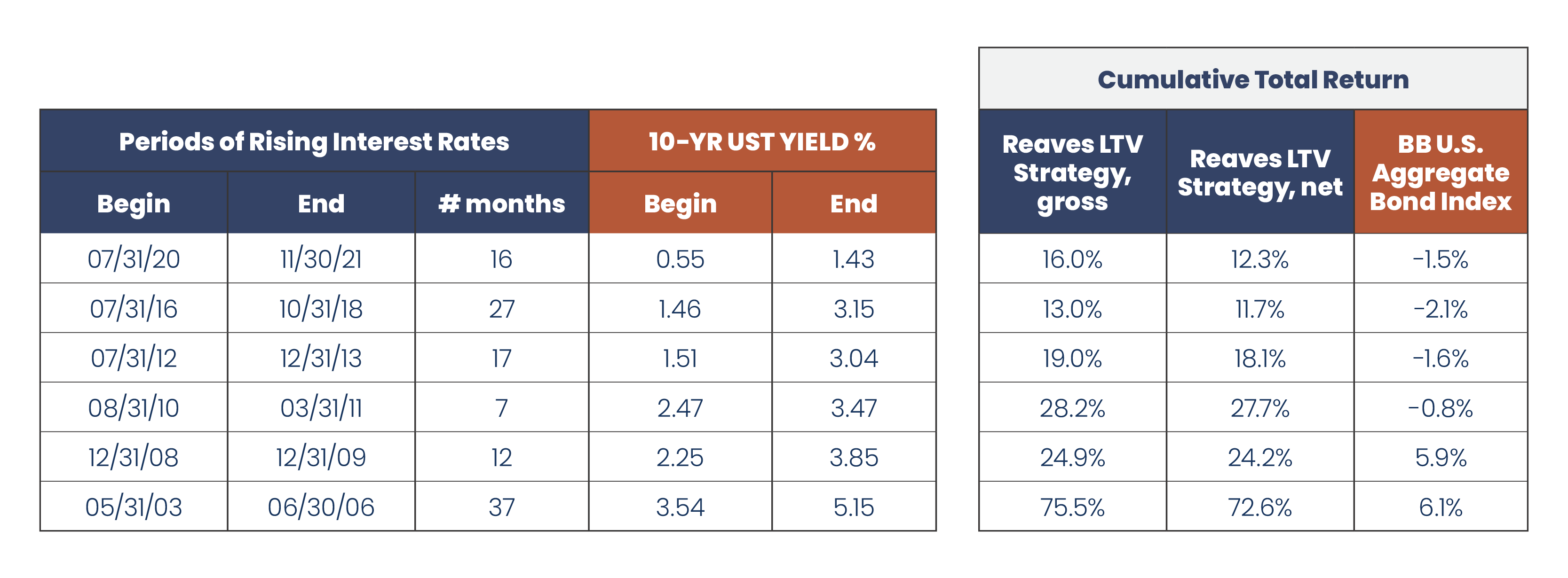

The table below puts this in perspective, again showing the returns of the Bloomberg Barclays U.S. Aggregate Bond Index alongside the returns of our flagship strategy in each of the rising rate environments that have occurred in the past 20 years.

Sources: eVestment, U.S. Federal Reserve, www.macrotrends.net

*For the period 7/31/20 to 11/30/21, Reaves’ LTV Strategy’s data (gross and net) is represented by our LTV SMA Wrap Composite; and for the period 12/31/77 to 10/31/18, Reaves’ LTV Strategy’s data (gross and net) is represented by our LTV ERISA Composite, which ended 12/20/19.

For more information about our composites, please see our disclosures.

While these tables help tell the story of the potential risk facing fixed income allocations, and how defensive strategies may help, we encourage you to gain further perspective by reading our investment brief, Rethinking 60/40: The Case for Defensive Equities.